It was late May 2016, The Right Hon. Member for Tatton, Mr George Osborne, published

an official HM Treasury analysis stating UK house prices would be lower by at

least 10% (and up to 18%) by the middle of 2018 compared with what is expected

if the UK remained in the European Union. So, eight

months on from the Referendum, are we beginning to show signs of that prophecy?

The simple answer is yes and no.

Good barometers of the housing market are the share

prices of the big UK builders. Much was made of Barratt’s share price dropping

by 42.5% in the two weeks after Brexit, along with Taylor Wimpey’s equally eye

watering drop in the same two weeks by 37.9%. Looking at the most recent set of

data from the Land Registry, property values in Mid Sussex are 0.42% down month

on month (and the month before that, they had barely grown with an increase of

only 0.33%) – so is this the time to panic and run for the hills?

Doom and Gloom then? Well, let me consider the

other side of the coin.

Well, as I have spoken about many times in my blog,

it is dangerous to look at short term. I have mentioned in several recent

articles, the heady days of the Mid Sussex property prices rising quicker than

a thermometer in the desert sun between the years 2011 and late 2016 are long

gone – and good riddance. Yet it might surprise you during those impressive

years of house price growth, the growth wasn’t smooth and all upward. For

example, Haywards Heath property values dropped by an eye watering 1.19% in May

2013 and 2.57% in April 2015 – and no one batted an eyelid then.

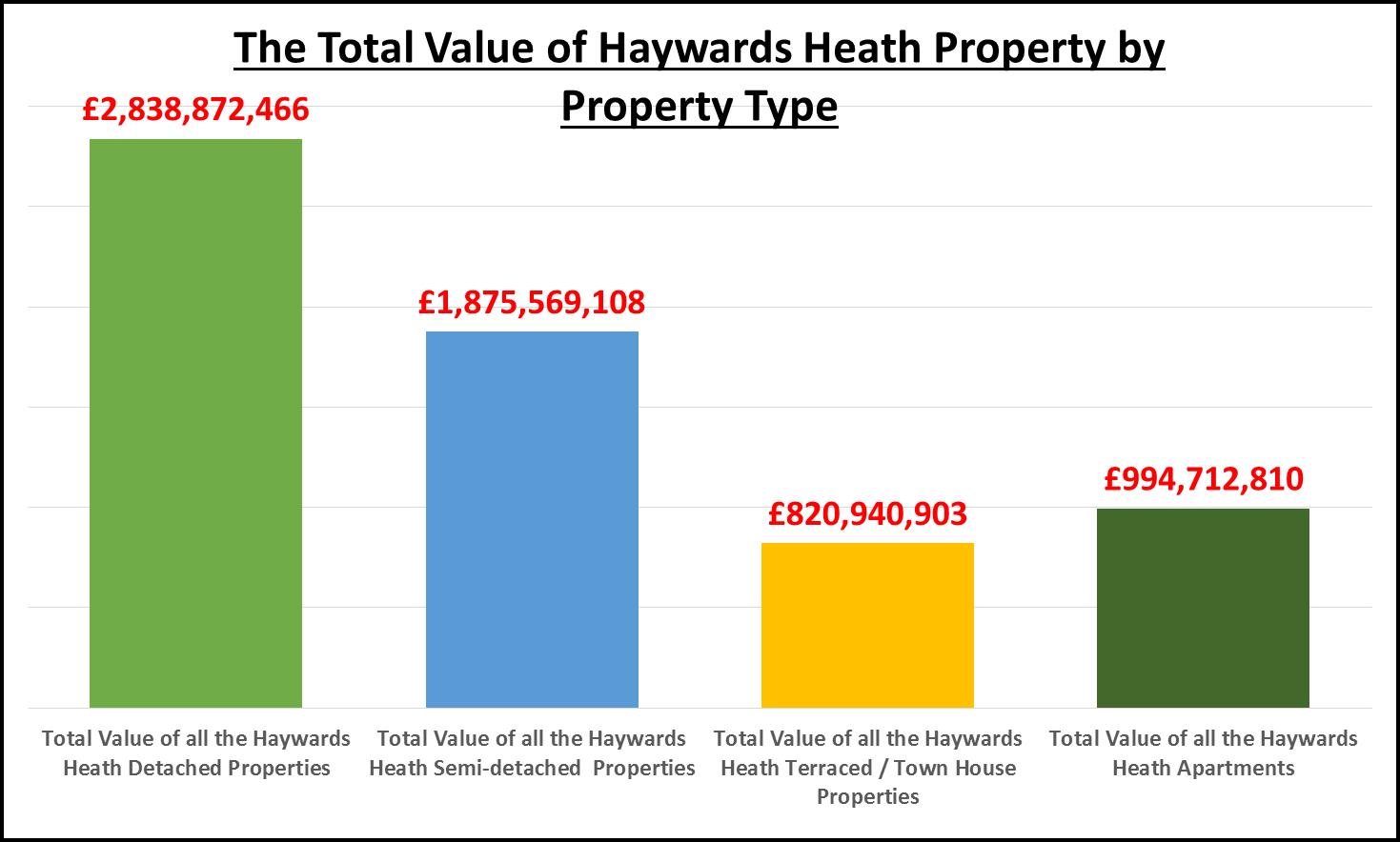

You see, property values in Haywards Heath are

still 10.23% higher than a year ago, meaning the average value of a Haywards

Heath property today is £474,950. Even the shares of those new home builders Barratt

have increased by 43.3% since early July and Taylor Wimpey’s have increased by

37.3%. The Office for Budget Responsibility, the Government Spending Watchdog,

recently revised down its forecast for house-price growth in the coming years -

but only slightly.

The Mid Sussex housing market has been steadfast

partly because, so far at least, the wider economy has performed better than

expected since Brexit. There is a robust link between the unemployment rate and

property prices, and a flimsier one with wage growth. Unemployment in the Mid

Sussex District Council area stands at 2,000 people (2.7%), which is considerably

better than a few years ago in 2012 when there were 2,800 people unemployed (3.8%)

in the same council area.

However, inflation is the only thing that does

worry me. Looking at all the pundits, it will get to at least 3% (if not more) in

the latter part of 2017 as the drop in Sterling in late 2016 renders our imports

with higher prices. If that transpires then the Bank of England, whose target for

inflation is 2%, may raise interest rates from 0.25% to 2%+. However, that won’t

be so much of an issue as 81.6% of new mortgages in the UK in the last two

years have been fixed-rate and who among us can remember 1992 with Interest

rates of 15%!